Why You Can’t Save Money: The “Next Month I’ll Save” Trap Every Indian Falls Into

About the Author: Sudarshan Mandal

Sudarshan Mandal is a SEBI-certified investor and an Electronics Engineer turned behavioral finance strategist. With 6+ years of active market experience and a professional background in Project Management, he applies a “failure analysis” lens to wealth creation.

After observing how even the most brilliant minds succumb to ego and volatility, Sudarshan founded Money Mandal to bridge the gap between academic theory and real-world behavior. His mission is to provide every investor with a mirror—allowing them to see their patterns, biases, and decisions with engineering-grade clarity.

If your salary disappears within 10–15 days every month, you’re not alone — and you’re not bad with money.

If your salary disappears within 10–15 days every month, you are not lazy, careless, or bad with money.

According to data and household surveys referenced by the Reserve Bank of India (RBI), a large percentage of Indian households struggle with consistent monthly savings, especially in urban middle-class segments.

You are probably stuck in one of the biggest middle-class money traps in India:

“This month is difficult. Next month I’ll save properly.”

The problem is that “next month” never comes.

Every month starts with good intentions:

- “This time I’ll save money from salary.”

- “This month I’ll spend less.”

- “After this one expense, I’ll become serious.”

But by the end of the month, your bank account is empty again.

If this sounds familiar, this blog will help you understand:

- Why you can’t save money every month

- Why middle-class Indians live salary to salary

- How to save money from salary in India

- A simple system to finally break the cycle

A Story Every Middle-Class Indian Will Understand

Ramesh is 31 years old and works in a private company in Mumbai.

He earns ₹45,000 per month.

On the 1st of every month, his salary comes. For a few hours, he feels rich.

He tells himself:

“This month I’ll finally start saving money.”

Then real life starts.

- ₹15,000 rent

- ₹5,000 EMI

- ₹4,000 credit card bill

- ₹3,000 groceries

- ₹2,500 Swiggy and Zomato

- ₹2,000 shopping because there is a sale

- ₹1,500 weekend outing

- Random small UPI expenses that don’t even feel important

By the 18th or 20th, his account balance is already low.

Then he says the same line again:

“No problem. Next month pakka save karunga.”

But next month, the same story repeats.

This is exactly how most middle-class Indians get trapped in a salary-to-salary lifestyle.

Why You Can’t Save Money from Salary in India

Most people think they cannot save because their salary is too low.

Sometimes that is true.

But in most cases, the real reason is not income.

The real reason is that we save whatever is left after spending.

And usually, nothing is left.

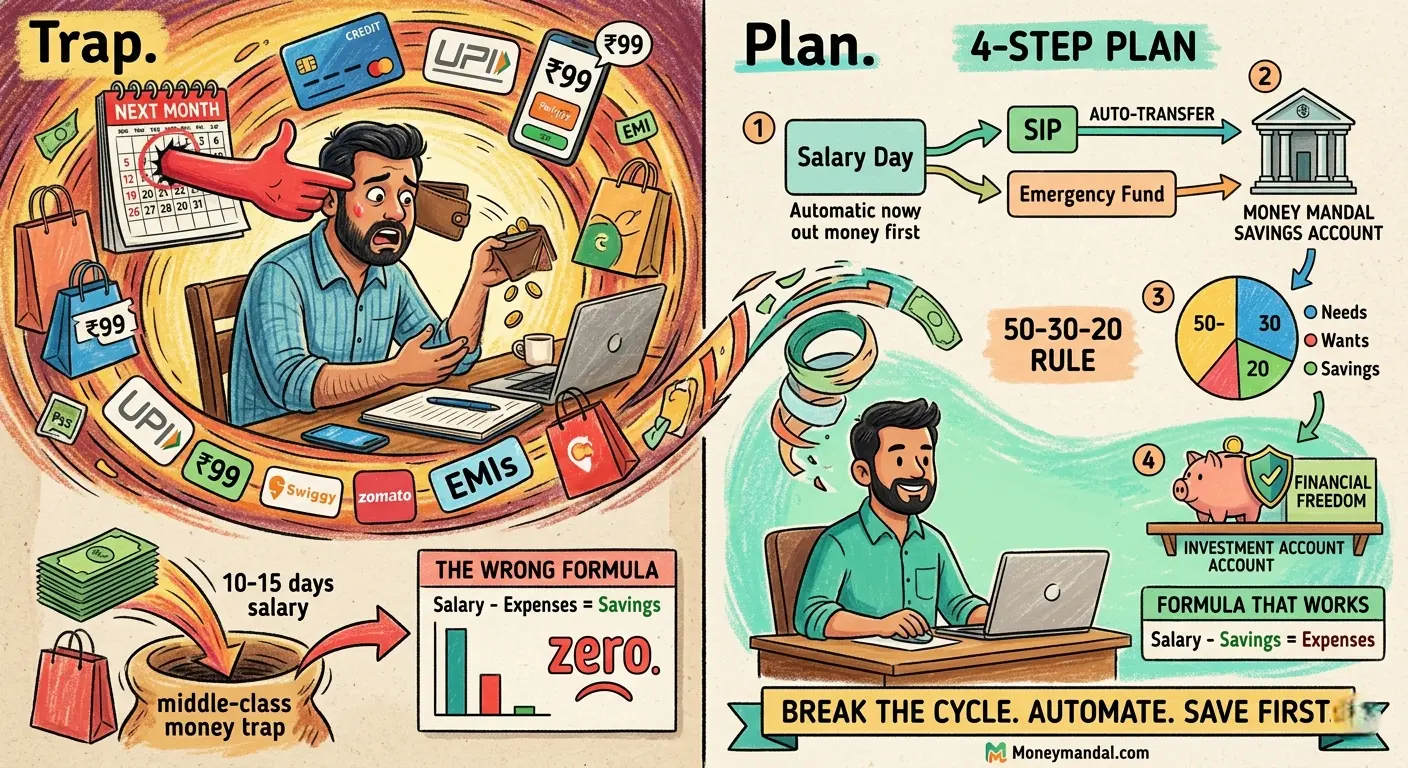

The Wrong Formula Most Indians Follow

Most people unknowingly follow this formula:

Salary – Expenses = Savings

The problem?

Expenses keep increasing.

So savings become zero.

The Formula That Actually Works

Instead, follow this:

Salary – Savings = Expenses

This one change can completely change your financial life.

5 Reasons Middle-Class Indians Fall Into the “Next Month I’ll Save” Trap

1. Lifestyle Increases Every Time Salary Increases

Whenever salary increases, expenses also increase.

- Better phone

- More online shopping

- More food delivery

- Bigger EMI

- Expensive weekends

This is called “lifestyle inflation.”

You earn more, but you still feel broke.

2. Emotional Spending Feels Like a Reward

After working hard the whole month, you feel you deserve something.

So you spend on:

- Food

- Shopping

- Trips

- Gadgets

There is nothing wrong with enjoying your money.

The problem starts when happiness today destroys your peace tomorrow.

3. Small UPI Payments Look Harmless

₹99 here. ₹149 there. ₹299 for food. ₹399 for shopping.

Individually, they look small.

But together, they quietly destroy your savings.

Many Indians spend ₹3,000–₹8,000 every month on “small” expenses without realizing it.

4. You Don’t Have a Clear Savings Goal

Saving feels difficult when there is no reason behind it.

If you are saving for:

- Emergency fund

- House down payment

- Child’s education

- Early retirement

Then saving feels meaningful.

Without a goal, money disappears easily.

5. You Keep Waiting for the “Perfect Month”

You think:

- “After bonus, I’ll save.”

- “After my loan ends, I’ll save.”

- “After my salary increases, I’ll save.”

But there is always another reason to delay.

The perfect month never comes.

The Hidden Cost of Not Saving Every Month

Let’s say you delay saving just ₹5,000 every month.

After 1 year, that is ₹60,000.

After 5 years, that becomes ₹3 lakh.

And if you had invested that money in a SIP, it could have become even more.

For example:

- ₹5,000 monthly SIP for 10 years

- At 12% annual return

- Total investment: ₹6 lakh

- Final value: Around ₹11.6 lakh

You are not only losing money.

You are losing:

- Time

- Compounding

- Financial freedom

How to Save Money from Salary in India: A Simple 4-Step Plan

If you have tried to save before and failed, do not try harder.

If you don’t know how to start, read this guide on how to save money from salary every month in India for a beginner-friendly step-by-step approach.

Create a better system.

Step 1: Save First on Salary Day

The moment your salary comes, transfer money immediately.

Even before:

- Rent

- Bills

- Shopping

- Food delivery

Take out at least 10%–20% first.

Example:

If your salary is ₹30,000:

- ₹3,000 goes into savings

- ₹2,000 goes into SIP

- Remaining ₹25,000 is for expenses

If your salary is ₹50,000:

- ₹5,000–₹10,000 should go directly into savings and investments

The earlier you remove it, the less likely you are to spend it.

Step 2: Automate Your Savings

The easiest way to save money is to remove the need to think.

Set up:

- Auto-transfer to another bank account

- Automatic SIP every month (learn more in our beginner guide on best SIPs for beginners in India)

- Recurring deposit if you are a beginner

Once it becomes automatic, saving stops feeling painful.

You can start with:

- ₹1,000 per month

- ₹2,000 per month

- ₹3,000 per month

The amount does not matter in the beginning.

Consistency matters.

Step 3: Use the 50-30-20 Rule for Indian Salaries

One of the best budgeting methods for middle-class Indians is the 50-30-20 rule.

If you want a deeper breakdown, read our detailed guide on the 50-30-20 rule explained for Indian families.

- 50% for needs

- 30% for wants

- 20% for savings

Example for ₹40,000 salary:

| Category | Amount |

|---|---|

| Needs | ₹20,000 |

| Wants | ₹12,000 |

| Savings | ₹8,000 |

If 20% feels difficult, start with 5%.

Then slowly increase it every few months.

Step 4: Keep Savings in a Different Account

Never keep savings in the same account where your salary comes.

Because if you can see the money, you will spend it.

Create:

- One salary account

- One savings account

- One SIP/investment account

This small trick works surprisingly well.

Real Example: Two Friends, Two Different Futures

Amit and Rahul both earn ₹40,000 per month.

Amit

- Keeps saying “next month I’ll save”

- Spends first

- Saves only if something is left

After 5 years:

- No emergency fund

- No investments

- Still stressed every month

Rahul

- Starts saving ₹3,000 every month from Day 1

- Increases savings slowly every year

- Starts one SIP of ₹2,000

After 5 years:

- More than ₹3 lakh saved and invested

- Less stress

- Better financial confidence

The difference is not salary.

The difference is system.

Why Most Saving Advice Fails

Most people say:

- “Spend less.”

- “Stop eating outside.”

- “Control yourself.”

But this advice does not work for long.

Because saving is not about motivation.

It is about making good decisions automatic.

You do not need more discipline.

You need a simple system that works even on your worst month.

7 Simple Ways to Save Money Every Month

- Save money on the same day salary comes

- Delete one unnecessary subscription

- Reduce food delivery to once a week

- Use cash for personal spending

- Avoid shopping during online sales

- Track every UPI expense for 30 days

- Increase savings by 1% every time your salary increases

These small habits can easily save ₹3,000–₹10,000 every month.

Why do I fail to save money every month?

Most people fail because they spend first and try to save later. By the end of the month, there is nothing left.

How much should I save from salary in India?

You should try to save at least 10%–20% of your salary. If that feels difficult, start with 5% and slowly increase it.

What is the best way to save money from salary?

The best method is to save automatically on salary day through SIPs, recurring deposits, or bank transfers.

What is the 50-30-20 rule?

The 50-30-20 rule means:

50% for needs

30% for wants

20% for savings

It is one of the easiest budgeting rules for beginners.

Can I save money even with a low salary?

Yes. Even saving ₹500–₹1,000 every month is better than waiting for a higher salary.

Final Reality Check

You are not one promotion away from becoming good with money.

You are one system away.

Stop saying:

“Next month I’ll save.”

Start saying:

“I will save first, then spend the rest.”

That one sentence can change your future.

Your 5-Minute Action Plan for Today

Before closing this page:

- Decide one amount you can save every month

- Open a separate savings account if you do not have one

- Set an automatic transfer for salary day

- Start one SIP, even if it is only ₹500

- Do not wait for next month

Start today.

Because the best time to start saving was yesterday.

The second-best time is today.

One year from today, you will either have savings… or the same excuse.