The Mind Behind the Money: Understanding Behavioral Finance

Have you ever held on to a losing stock far longer than you should have, whispering to yourself that it would “just get back to your purchase price” before you sell? Or perhaps you’ve felt that sudden, electric urge to buy into a trending crypto coin or a “meme stock” simply because your entire social media feed seemed to be celebrating overnight gains?

If you’ve ever made a financial decision that felt more emotional than logical, you’ve already experienced Behavioral Finance in action.

At Money Mandal, this concept sits at the heart of everything we do. We believe that mastering money is not just about understanding market cycles—it’s about understanding the biological and psychological machine making the decisions: your brain.

In this comprehensive guide, we’ll explore the fascinating intersection between psychology and economics, why traditional finance often fails to explain real market behavior, and how your own subconscious might be the biggest influence on your financial destiny.

1. What Exactly Is Behavioral Finance?

For decades, academia treated finance almost like physics—precise, mathematical, and governed by universal laws. Financial models were built on the assumption that markets are efficient and people are logical.

But reality kept contradicting the theory.

Markets consistently experienced bubbles that shouldn’t exist, crashes that happened without warning, and irrational rallies driven by nothing but hype. Traditional models couldn’t explain why a stock’s price would double in a week despite no change in the company’s earnings.

Behavioral finance emerged in the late 20th century to bridge this gap. It asks a simple, revolutionary question: What happens when real human psychology meets financial markets?

Unlike traditional finance, which focuses on what investors should do (the “Optimal” path), behavioral finance focuses on what investors actually do (the “Real” path). It acknowledges that our choices are frequently driven by a cocktail of emotions:

- Fear: The instinct to flee when prices drop.

- Greed: The desire for “easy money” that blinds us to risk.

- Pride: The inability to admit we were wrong about a trade.

- Regret: The pain of missing out on a gain or realizing a loss.

- Overconfidence: The belief that we are smarter than the average participant.

2. The Great Divide: Rationality vs. Reality

To understand why behavioral finance is the cornerstone of modern investing, we need to examine the “Standard Finance” model it challenged.

Traditional Finance: The “Rational Investor”

Traditional theories, such as the Efficient Market Hypothesis (EMH), assume that investors are “Econs”—mythical creatures who have perfect self-control and process all available information instantly. In this world:

- Investors are perfectly rational.

- Markets instantly reflect all available information.

- People always act in their long-term best interest.

- The Result: Asset prices always reflect “fair value,” and “beating the market” is nearly impossible.

Behavioral Finance: The “Human Investor”

Behavioral finance starts with a much more grounded assumption: Investors are human. Humans operate under Bounded Rationality. We have limited time, limited information, and limited brainpower.

Because we can’t calculate the complex probability of every outcome, our brains use Heuristics—mental shortcuts—to make quick decisions. While these shortcuts helped our ancestors survive a predator on the savannah, they are often disastrous when trying to price a tech stock.

3. The Pioneers Who Changed Everything

The shift from “Physics-Finance” to “Psych-Finance” was led by researchers who realized that the “Invisible Hand” of the market was actually attached to an emotional human arm.

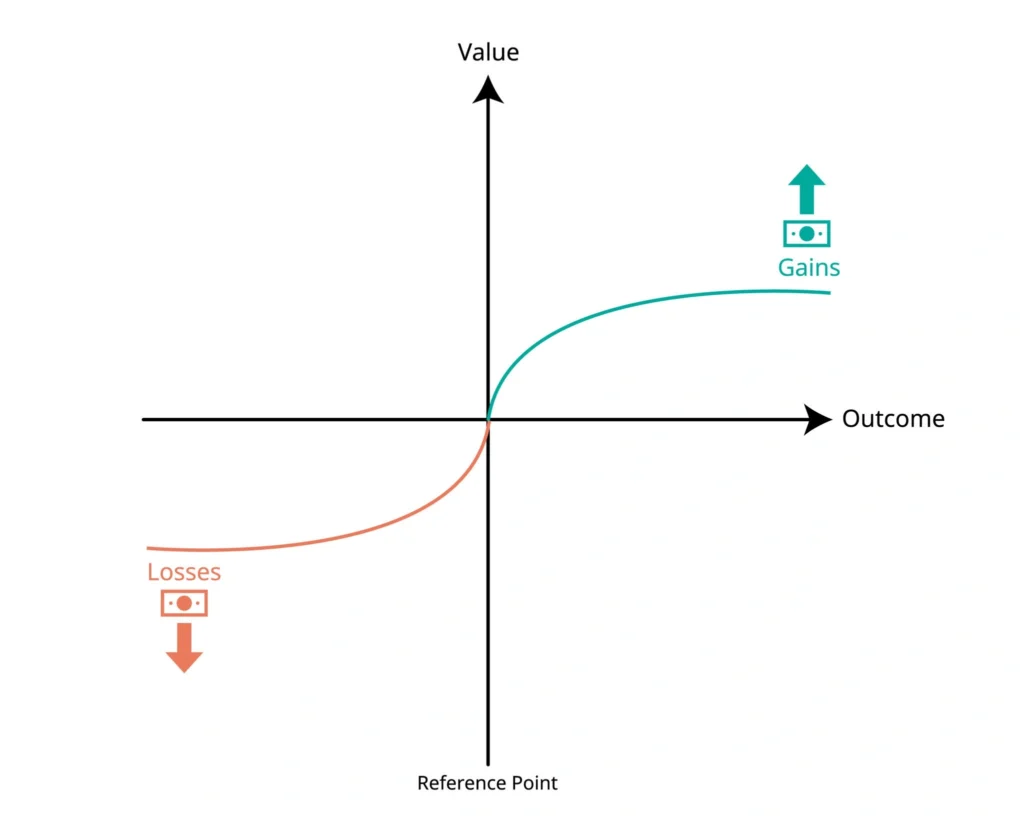

Daniel Kahneman and Amos Tversky: Prospect Theory

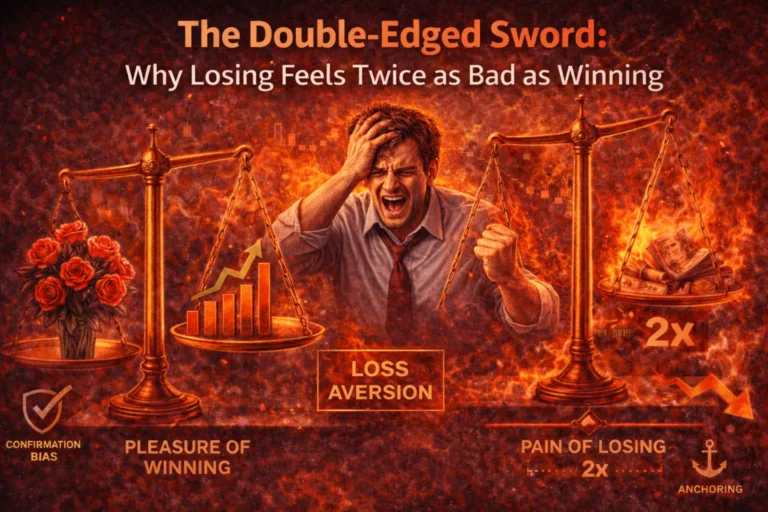

In the 1970s, psychologists Daniel Kahneman and Amos Tversky introduced Prospect Theory, which eventually won Kahneman the Nobel Prize. Their most significant discovery was Loss Aversion.

They proved that the pain of losing ₹10,000 is psychologically twice as powerful as the joy of gaining ₹10,000. This asymmetry is why you feel a “pit in your stomach” during a market dip, even if your long-term gains are still high. It’s why investors hold losing stocks for years (to avoid “realizing” the pain) but sell winners too early (to “lock in” the fleeting joy).

Richard Thaler: Mental Accounting and Nudges

Richard Thaler, another Nobel laureate and author of Nudge, explored how we categorize money. Through Mental Accounting, he showed that humans treat money differently depending on its source.

Example: You might spend a ₹5,000 “birthday gift” on a luxury dinner, yet spend three hours researching the best price for a ₹5,000 microwave using your “salary” money.

Logically, money is fungible (one rupee is the same as any other). Psychologically, we treat “found money” or “investment gains” like “House Money,” often taking reckless risks we wouldn’t take with our hard-earned savings.

4. How Psychology Affects Trading Decisions

Our biology is ill-equipped for the digital ticker tape. Two specific psychological phenomena dominate daily trading:

The Action Bias

In times of stress, humans feel a primal urge to do something. If you see a red candle on a chart, your “fight or flight” response kicks in. In the stock market, “doing something” usually means overtrading. Rationality tells us that for long-term wealth, the best move is often to sit on our hands. Psychology, however, demands that we “regain control” by hitting the sell button.

The Framing Effect

The way a choice is “framed” changes the choice itself.

- “This strategy has an 80% success rate.”

- “This strategy has a 20% failure rate.”

Even though the math is identical, investors overwhelmingly flock to the first statement. Wall Street marketing relies on the Framing Effect to make risky products look like safe opportunities by highlighting the “upside” frame.

5. The Most Powerful Biases in the Market

If you want to improve your returns, you must first identify these four “Portfolio Killers”:

I. Herd Behavior (Social Proof)

Humans are social animals. In the wild, if the tribe starts running, you run. In the market, this creates Bubbles and Panics. The “Fear Of Missing Out” (FOMO) drives people to buy at the top, and “Social Proof” makes people sell at the very bottom.

II. Overconfidence Bias

Surveys show that roughly 80% of traders believe they are “above average.” Mathematically, this is impossible. Overconfidence leads to underestimating risk, ignoring “stop-losses,” and believing that your “gut feeling” is better than the data.

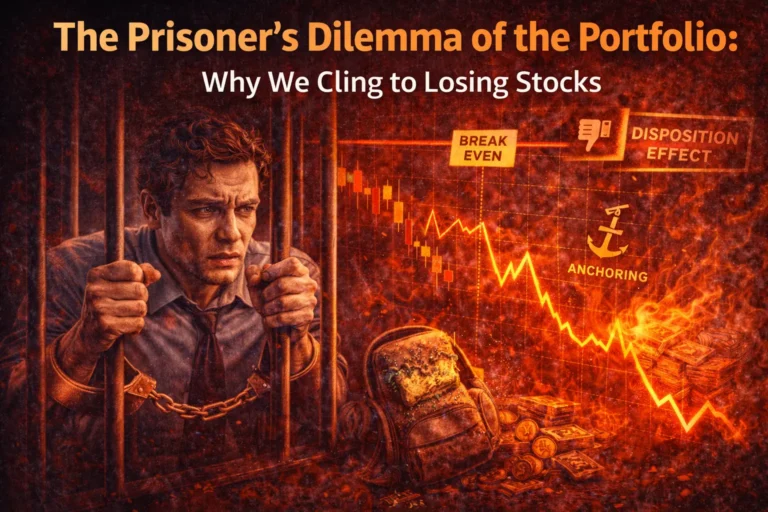

III. Anchoring Bias

Anchoring happens when you fixate on a specific number—usually your purchase price.

- The Trap: You buy a stock at ₹500. It drops to ₹300 because the company’s business model has failed. Instead of selling to save your remaining capital, you “anchor” to ₹500 and refuse to sell until you “break even.”

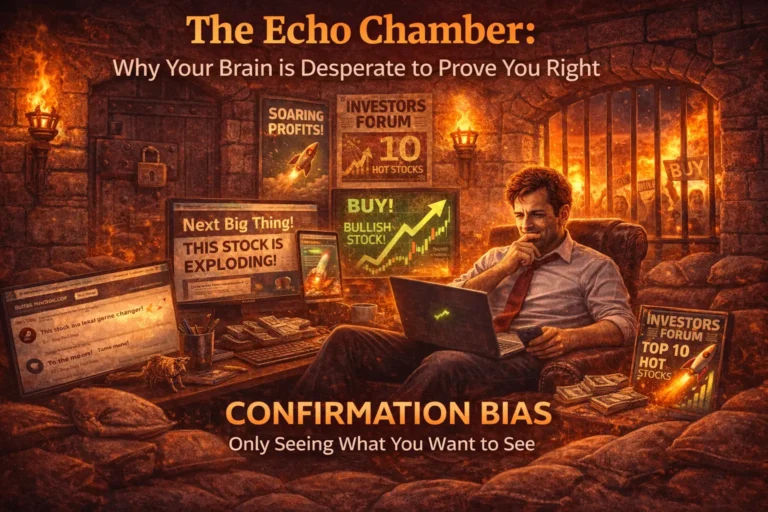

IV. Confirmation Bias

We love being right. We naturally seek out YouTube videos, news articles, and tweets that agree with our current positions. If you are “Long” on a company, you will likely ignore negative earnings reports and label them as “manipulation,” while celebrating any minor positive news. This prevents us from seeing the “exit signs” until it’s too late.

6. How Biases Move Entire Markets

When millions of investors experience these biases at once, we see Market Anomalies:

- Market Bubbles: Herd behavior and overconfidence drive prices into the stratosphere, far above any logical valuation.

- Panic Selling: Loss aversion and the action bias turn a small correction into a full-blown crash.

- Volatility: Emotional reactions to news causes prices to swing much wider than the actual change in a company’s value.

7. Why Behavioral Finance Matters for YOU

You cannot “turn off” your emotions. You can, however, build a system to manage them. Understanding these biases doesn’t make you a robot; it makes you an informed human who is less irrational than the crowd.

That “irrationality gap” is where the profit lies. Investors who recognize their biases can:

- Build structured decision processes.

- Avoid impulsive, emotional trades.

- Manage risk based on math, not “feelings.”

- Stay disciplined when everyone else is panicking.

8. Why Money Mandal Exists

At Money Mandal, we believe financial success is 20% head-knowledge and 80% behavior. Most investors spend years learning technical indicators and valuation methods, yet they still fail because they can’t manage their own minds.

That is why we created tools like MandLy—a behavioral decision tool. MandLy is designed to help you track not just what you bought, but why you bought it.

- What was your mood? * What was your “exit plan” before the emotions kicked in? * Were you following a tip or a trend?

By recording your emotional state alongside your trades, you begin to see the patterns of your own mind. Awareness is the first step toward discipline.

Conclusion: The Real Battle Happens in Your Mind

The most important asset in your portfolio is not a stock, a bond, or a fund. It is your decision-making process.

Behavioral finance teaches us that the greatest risk to your wealth isn’t the market—it’s the person in the mirror. When you learn to recognize loss aversion, anchoring, and the herd instinct, you gain the power to build systems that protect you from yourself.

The goal is not to eliminate emotion; that’s impossible. The goal is to make better decisions despite them.

A Simple Behavioral Checklist Before Every Trade

Before you hit that button, take 60 seconds to run through these questions:

- The “Why” Test: Am I buying this because of data/strategy, or because I’m afraid of missing out on a trend?

- The Opposite View: What is the strongest reason someone would sell this stock right now? Do I have an answer for that?

- The 10-10-10 Rule: How will I feel about this trade in 10 minutes? 10 months? 10 years?

- The Pre-Mortem: If this investment goes to zero, what would be the most likely cause? Can I live with that possibility?

- The House Money Check: If I had to work 100 hours of overtime to earn this specific amount of money, would I still be this “aggressive” with it?

Understanding behavioral finance is the first step toward wealth. The next step is observing your own behavior in real-time. Because in the markets, the greatest edge is not predicting the next price move—it is mastering the psychology behind your own.

Ready to start your behavioral journey? Start logging your trades with Money Mandal’s D Log today.

If traditional finance is “logical,” why do I need behavioral finance?

Traditional finance assumes everyone is a “rational machine” who always makes the perfect choice. In reality, humans are driven by emotions like fear, greed, and overconfidence. Behavioral finance bridges this gap by explaining why we make “irrational” mistakes—like holding a losing stock for too long or buying into a hype-driven bubble. Understanding this gives you an “irrationality edge” over the rest of the market.

What is “Loss Aversion,” and how does it hurt my portfolio?

Loss aversion is the psychological finding that the pain of losing money is twice as powerful as the joy of gaining it. This bias often tricks investors into two dangerous behaviors:

Refusing to sell a losing stock because they don’t want to “realize” the pain.

Selling winning stocks too early just to “lock in” a small sense of relief. Recognizing this allows you to stick to your original strategy rather than reacting to the “pit in your stomach.”

Can I ever truly “turn off” my emotions when trading?

No, and you shouldn’t try to. Emotions are a hardwired part of the human brain. The goal of behavioral finance isn’t to turn you into a robot, but to help you build a system to manage those emotions. By using frameworks like the “10-10-10 Rule” or a “Pre-Mortem,” you create a buffer between your emotional impulse and your financial action.

How does the Money Mandal “MandLy” help me become a better investor?

Most investors only track their profits and losses, but they never track their mindset. The MandLy helps you record your mood, your “why,” and your exit plan before the market gets volatile. Over time, this data reveals your personal patterns—like if you tend to overtrade when you’re stressed—allowing you to fix the “person in the mirror” before they make a costly mistake.